Impending sea change in monetary policy

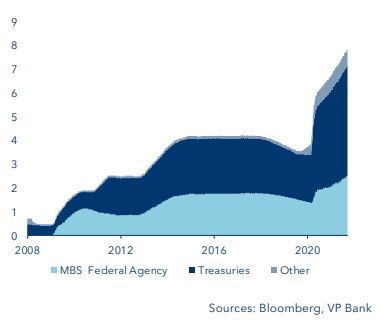

The “taper” is imminent in the USA as there is no longer any need for the Fed to stick with the ultra-expansive monetary policy it introduced in response to the pandemic’s economic consequences. That strategy has resulted in a doubling of the central bank’s bond holdings, which currently stand at nearly USD 8 trillion (see chart).

Federal Reserve securities holdings, in USD trillion

Meanwhile, US gross domestic product (GDP) has returned to, and even exceeded, its pre-crisis level. Moreover, fiscal policy is also very expansionary and inflation risks are on the rise. The shortage of intermediate goods and raw materials has taken on huge dimensions, with US producer prices recently increasing by an annualised 8.3%. The surge in energy costs is particularly disturbing. Granted, the price of natural gas in the States has risen far less sharply than in Europe thanks to America’s self-sufficiency; nonetheless, it has tripled year-on-year.

Although consumer price inflation should retreat significantly from the current 5%+ level, the question remains as to where it will actually come to rest in 2022. Thus it should come as no surprise that not just the Fed, but also the ECB and other major central banks are starting to talk about heightened inflation risks.

The monetary authorities are sensing the need for action on their part, despite the risks to the global economy posed by today’s material shortages. They have at their disposal well-stocked toolboxes that make it possible to pull off the delicate balancing act between inflation and economic disruption. For example, a tapering off of the Fed’s monthly securities purchases will not cause the US economy to stumble, but it does send a clear signal that the central bank will not stand idly by as inflation risks increase.

The Fed is dealing with the situation

The September FOMC meeting minutes made it patently clear: the US economy has come closer to hitting the Fed’s employment and inflation targets, which in turn justifies a reduction of its asset purchases. Chairman Jerome Powell hinted that tapering will on the agenda at the FOMC meeting scheduled for 2-3 November, going so far as to say that bond purchases could be completely discontinued already by the middle of next year. This pace would be much faster than the previous taper eight years ago, when the Fed took all of ten months (December 2013 until October 2014) to complete the task.

Since this past June, the Fed has been buying securities at a net monthly rate of USD 120 billion. Were it to spread the reduction evenly over eight months (assumption: start in November, end in June), the monthly volume would have to be reduced by around USD 15 billion. Also conceivable is a taper that would begin gently and then gradually increase in size. However, that strategy strikes us as being unlikely since the Fed would then need to step on the brakes too hard in 2022. In the previous taper, the Fed also took an even-handed approach in trimming its monthly purchases, namely by USD 10 billion a shot.

How will things go after the taper?

Following the taper, the Fed will probably leave its balance sheet total unchanged at least for a while and merely reinvest the proceeds from maturing issues as its focus returns to more conventional measures. The FOMC’s projections published in September imply that the members envisage an initial rate hike already in 2022. By logical extension, this suggests that the first rate move could actually take place shortly after the taper is concluded. This, too, would indicate that the Fed intends to recalibrate at a much faster pace than it did back in October 2014, when the initial post-taper hike followed only in December of 2015.

According to the aforementioned projections, the Fed funds rate could rise to one per cent by the end of 2023, which would involve three 25bp rate bumps. So it would appear that the Fed is in somewhat of a hurry. The rapid economic recovery and heightened inflation risks are indeed being taken into account in the central bank’s monetary policy deliberations.

How the financial markets react(ed)

Even before the Fed made its first tapering move in 2013, bond yields skyrocketed in an episode that has gone down in financial market annals as the “taper tantrum”. However, seemingly blind to the whole affair, the equity markets continued to march higher. And nothing changed in that respect, even in the face of the rate hikes that were ultimately introduced in late 2015. The reason: Tapering simply means that the monthly bond purchases are being reduced, yet the Fed's balance sheet grows further as the economy continues to receive monetary support. It is precisely this fact that keeps the financial markets happy. Equally spoken, the current rise in yields is likely to persist this time around. The long end of the yield curve also reflects market expectations at the short end. In other words, since tapering signals that the Fed intends to raise interest rates at some point in the future, we believe that yields on longer-dated Treasuries will rise gradually, with 10-year T-bonds initially taking aim at the 2% mark.

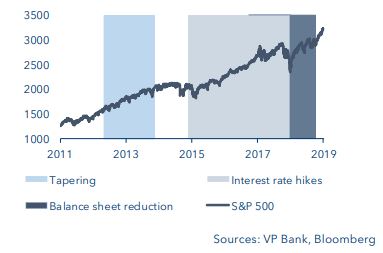

A glance back at the previous monetary tightening cycle reveals that the financial markets only then started to unravel once the Fed’s balance sheet was shrinking in tandem with rising interest rates. The balance sheet slimdown commenced in October 2017 when the central bank stopped reinvesting the proceeds from redeemed issues. Initially, the diet started with a USD 10 billion monthly reduction and then gradually increased by increments of USD 10 billion to a point where the balance sheet total was shrinking by USD 50 billion each month until the process was completed in September 2019. The associated reduction in the money supply was temporarily reflected by higher risk premiums in the money markets, which in turn caused a spike in equity market volatility. In general it can be said that the interest rate sensitivity of stocks has increased in recent years, seeing as how the overall valuation level is relatively high and the share of growth stocks has also risen. In short, the real stress test will come only once the money supply starts to drop.

S&P 500 and monetary policy, 2013 > 2019

Also in terms of USD, monetary tightening does not necessarily go hand in glove with a stronger greenback: during the 2014 taper, the US dollar actually lost a bit of ground against the euro. Admittedly, USD managed to make considerable headway against the European common currency at the end of 2014 in anticipation of Fed interest rate hikes. But it then gave back some of those gains in the period between early 2017 and mid-2018 – at times even suffering sizeable losses despite the fact that the Fed was actually trimming its balance sheet.

Moreover, during the aggressive tightening phase between 2004 and 2007 when the Fed funds rate was bumped from 1% to 5.25%, the broad US dollar index shed roughly a quarter of its value. Against EUR it lost almost 30% during that time frame, and this even though the ECB was tightening to a considerably lesser extent.

Our point here is that no hasty conclusions regarding the dollar should be drawn merely on the basis of a tighter US monetary policy. Much to the contrary, the greenback tends to weaken in times of global economic vibrancy, irrespective of the Fed’s monetary policy stance. By the same token, an economic downturn accompanied by heightened jitters in the financial markets tends to boost the US currency, given the dollar’s traditional reputation as being a safe haven.

What does the ECB have in mind?

The European Central Bank will not toe the line with the Fed. Although the ECB’s Governing Council has decided to reduce the PEPP-related securities purchases, this should not be understood as “tapering”. In the second and third quarters of 2021, the ECB did increase its purchases in order to absorb the unusually large volume of maturing eurozone government bond issues. So it is merely going back to the normal level. We reckon that the European monetary authorities will discontinue the PEPP programme on schedule in March 2022; however, unconfirmed rumours have it that the Frankfurt central bankers are contemplating a replacement for PEPP. In view of today’s rising inflation rates, we do not consider a new purchase programme to be opportune. But putting an end to PEPP does not mean that the ECB will do without the other quantitative measures in its toolbox. Ever since 2015, bond buybacks have been under way in parallel to PEPP, namely in connection with the Asset Purchase Programme (APP), and this to the tune of EUR 20 billion per month. ECB chief Christine Lagarde intends to keep APP going after the discontinuation of PEPP. Thus the financial markets’ expectation of an initial interest rate hike towards the end of 2022 or the beginning of 2023 is, to our way of thinking, overly ambitious. We are looking for the ECB to make its first move at the earliest in H2 2023.

Summary

The days of ultra-expansive US monetary policy are numbered. The Fed can be expected to reduce its monthly securities purchase volume starting in November. The ECB, on the other hand, will take its time before making an about-face. The Fed’s modest tightening does not necessarily mean that the equity markets take a hit or that USD appreciates. Only when the Fed stops reinvesting the proceeds from maturing securities and withdraws liquidity from the system should investors start to reckon with rough seas.

Download

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notes_en.pdf