Economy and markets under shock from pandemic

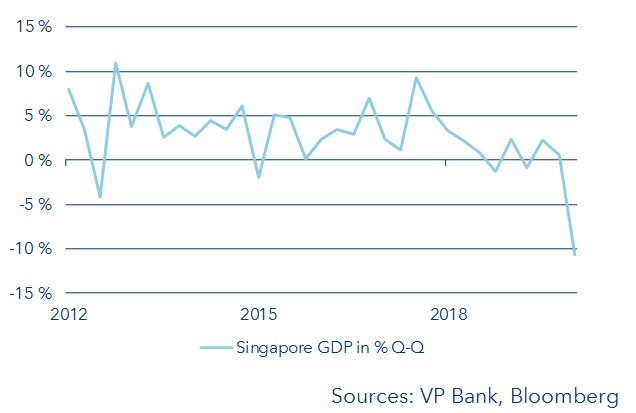

COVID-19 had led to a worldwide standstill in economic activity. Just how steeply the declines in gross domestic product (GDP) might be is currently a matter of considerable forecasting uncertainty, but we shall nevertheless venture an initial assessment. Although the first quarter of 2020 got off to a good start, the situation took a dramatic turn in February. This means that the economic growth in January and partly in February compensated to a certain degree for the losses in the second half of the quarter. For the US, we currently estimate that Q1 GDP will decline by 0.2% versus the previous quarter, while the April to June quarter is looking more like a drop of 7.8%. Extrapolating these figures to the entire year, we arrive at a slump of roughly 30%. Using Singapore as an example, it becomes clear just how much an economy can collapse. The city-state, which is highly dependent on international trade, already recorded a Q1 decline in GDP of 10.6% compared to the Q4 reading for 2019. In that the novel coronavirus was spreading rapidly in Asia already at the beginning of the year, the economic consequences were felt there earlier than in the West.

Singapore GDP: an example for other countries

The economic pattern we expect to see in the USA can be applied to other national economies practically at will, give or take a few percentage points. In the eurozone, the GDP retreat will be more severe already in the first quarter, merely because the virus struck earlier on the European continent. As to the second quarter, the losses here are likely to be somewhat smaller than in the US, mainly due to the well-developed social security systems and (depending on the given country and industry) strong trade unions and employer associations. The social partners are experienced and created a number of crisis mechanisms that today are proving to have a stabilising effect. These include plant closures based on furloughs, short-time work and working hours accounts.

Will the aid packages actually help?

Across the globe, central banks and governments have responded to the crisis by announcing aid packages. This time, though, the rescue measures are not economic stimulus programmes. The actions taken thus far – the US government, for example, has cobbled together a package worth more than USD 2 trillion – will only prevent the worst, i.e. a collapse of the entire economy. Due to the limited scope of the existing US social security system, these added government funds will provide important support for large cross-sections of the population. Not just in the USA, but everywhere, government lending and guarantee programmes are targeting micro-enterprises in particular to prevent liquidity shortfalls. The billions in aid are intended to help the national economies get through the coming weeks and months in the best possible way. This is of crucial importance. If there were to be a huge wave of insolvencies, there would be too few companies in a position to drive the recovery once the coronavirus has been conquered. In other words, if too many companies and businesses go belly-up at this point, there can be no upturn at some later date.

Will the recovery be a rapid one?

Far more decisive than the extent of the slump will be how quickly the global economy can recover from this epochal exogenous shock. The question is whether the course of the economy will resemble a V or a U – or in worst case, even an L. The latter obviously implies that the economy does not gain a foothold for an extended period of time. At present, we expect the economy to develop in a U-shaped fashion, i.e. with a sharp slump followed by a hesitant yet gradually accelerating recovery. In the USA as well as in Europe, attempts will presumably be made to ramp-up industrial production step by step, and as soon as possible. Restaurants, hotels and major sporting and cultural events are likely to remain affected by the ban on interpersonal contact and the corresponding restrictions for some time to come. If the strict “social distancing” measures were to be relaxed overnight, there is the threat of a renewed rise in the number of infected persons and hence a second wave of the disease. For this reason, we consider a V-shaped economic path – i.e. a sharp slump followed by a rapid recovery – to be unlikely. Moreover, numerous insolvencies are almost inevitable in our view. The central bank and government aid programmes should prevent an enormous wave of bankruptcies, but it is unrealistic to think there will be none at all. We therefore reckon that overall economic growth rates will return to positive territory in the second half of the year, although that growth is likely to be relatively modest. For the USA, this means: Although our calculations suggest that the August-to-September period will show nothing more than a breakeven in terms of GDP, a quarter-on-quarter growth rate of 3.2% could be in the making for the fourth quarter.

Dramatic decline in corporate profits

What we are witnessing at the macroeconomic level is no different than the happenings at listed companies. They need to reckon with a collapse in their sales and profits. There are headwinds blowing from several directions at the same time. On top of the slump in final demand, companies are also experiencing massive disruptions in their supply chains, which in turn will lead to production stoppages or at least to higher costs attributable to supply-side pinch points. For the first time, especially the large companies typically represented in the stock market are now also experiencing the flipside of the global division of labour and specialisation.

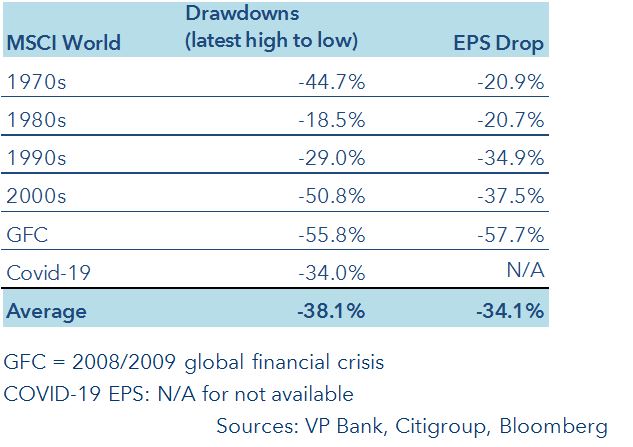

Our outlook for the development of GDP estimates that the effects of COVID-19 will come full-bore mainly in the second quarter. In terms of Wall Street, we expect that companies will in fact record losses across the board. As to the year as a whole, we foresee what could be roughly a one-third drop in corporate profits. European companies are likely to be hit even harder at least optically (due to the MSCI Europe’s more cyclical sector mix). Such a collapse in earnings is rare, so there are few comparables. The largest slump in corporate earnings to date was recorded during the financial crisis (see table).

Price and profit collapses (global stocks)

As mentioned, a profit collapse of this magnitude is rare, just like bear markets. A decline of more than 20%, as witnessed in practically all stock markets in recent weeks, traditionally marks the start of a bear market. So far this has only happened once every decade. Far more frequent are small and moderate price setbacks. Emotions play an important role in the extent of the losses, but unlike interim corrections, in a bear market there is a close correlation between price developments and profit developments – an examination of previous bear markets reveals that the respective share price loss corresponded almost exactly to companies’ subsequently reported profit declines. The exceptions can be explained by the high inflation in the 1970s and the exorbitant valuations at the turn of the century upon the burst of the dot.com bubble.

Is the worst already behind us?

The US equity market has meanwhile dropped 34% from its all-time high recorded only five weeks ago. In the past several sessions, it has been able to recover somewhat. So if the aforementioned correlation between bear markets and earnings remains intact, and if we compare our anticipated decline in US corporate profits with the maximum price slump, it becomes clear that the stock market has reacted appropriately. As dramatic as the dynamics have been, today’s low prices appear to be entirely justified in view of the currently projected economic damage. And meanwhile, the valuations based on anticipated future earnings are not (yet) particularly favourable.

Thus we consider it premature to speak of a turning point. Equity markets do have the “talent” to anticipate future happenings before they are even confirmed in the form of better news or an actual rise in profits. After the last financial crisis, for example, corporate earnings bottomed out in January 2010. At that time, share prices were already 50% higher than their lows recorded in March 2009.

But this time around, things are a bit different. The modern financial markets have never experienced a pandemic shock like the one we are currently experiencing. The lack of comparability with earlier periods is causing many investors to keep their powder dry. Moreover, the market is still busy trying to put its head around the current situation. A glance at the consolidated expectations of equity analysts shows that we are only at Square 1 right now. They have adjusted their estimates only hesitantly and still project a slight increase in earnings.

We expect that an ongoing mix of wishful thinking and fearful action will result in another downside leg. In addition to news on the medical front, doubts will arise as to whether the government measures are actually sufficient and will take effect quickly enough. And then of course there is the open question about how the crisis will affect the debt market. If all these worries coalesce simultaneously, it is to be feared that the equity markets will retreat to their recent lows, or even beyond.

But things could also turn out differently

Equally spoken, one could well imagine scenarios that make the worst fears evaporate instantaneously. Such would be the case, for example, if pharmaceutical research achieved a rapid breakthrough with a therapeutic drug. According to the World Health Organization (WHO), 41 clinical trials of vaccine against the novel coronavirus have been initiated worldwide. The good news is that researchers are not starting from scratch. They are already familiar with other corona viruses such as MERS (outbreak in 2012) and SARS (outbreak in 2002/03). This is why diagnostic tests have been introduced and performed relatively quickly. The situation is similar in the field of drug research. If an antiviral drug or vaccine were to be officially approved in the coming weeks, this could open the door for a rapid economic recovery – and in the same vein, the personal distancing/isolation measures could be relaxed more quickly. Although companies would still have to swallow a significant drop in short-term profits, the financial markets would probably mount a sustained recovery. The latter in particular would be very good news for the real economy: the sooner the tensions in the capital markets ease, the better the credit channels and liquidity supply will function.

Alas, at the other end of the spectrum, this upbeat scenario is contrasted by an economic trend similar to the letter L. Were that to be case, the deep slump in the second quarter would not be followed by a recovery – and something with the look and feel of an economic depression could evolve. In this scenario, the virus would maintain its bear hug on the world, at which point a major wave of insolvencies cannot be ruled out. Prolonged stagnation and further declines in economic dynamism would then be on the daily docket. Stress levels would naturally spike, not only in the stock markets, but especially in the credit markets.

Recommendation

In their uncanny way, the financial markets were exceptionally quick to price in the far-reaching, negative developments that lie ahead for the real economy. The massive slump in growth, especially in the second quarter, will exceed anything the tentative growth in the second half can counteract. This will naturally have a profound impact on corporate profits. The profit decline we are anticipating has been largely reflected in current share prices. However, we do not yet view this as being a turning point.

We consider another round of temporary setbacks to be more likely than a steady market recovery. In the wake of the recent wave of selling and sharp reflex rallies, investors and analysts alike will continue to be preoccupied processing the events and new news in the coming days and weeks.

Against this backdrop, investors are well advised to proceed with caution. A potential further stock market rally should not automatically be confused with a sustainable bottom-building process. That said, we recommend remaining invested. If one sells now, there is the risk of missing the best time for re-entry. We would continue to focus on high-quality companies with strong balance sheets. This applies equally to stock as well as bond selection. And broad diversification also means including non-cyclical asset classes such as gold and insurance-linked securities.

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notes_en.pdf

Add the first comment